Use our Partnership Agreement template to detail the terms of a business partnership.

Updated November 3, 2023

Written by Josh Sainsbury | Reviewed by Brooke Davis

A partnership agreement is a legal contract between business partners that defines their roles, responsibilities, and how profits and losses are distributed, used to prevent disputes and protect the partners’ interests in the business.

Using a Partnership Agreement template means you and your new business partner will have an agreement you can rely on and be confident that your requirements are met.

Outline all the key information of a partnership that has general and limited partners.

Use this template to detail the key information if your partnership will have members with limited liability.

If you're looking to go into a partnership to buy or manage real estate then detail the key elements in our Real Estate Partnership Agreement.

Use this template if you want to equally share all profits and losses with a partner.

Use this template to detail the key information of a partnership for a small business.

Use our partnership dissolution agreement to protect your interests and assets and to provide clarity and protection for all parties involved.

A Partnership Agreement is an internal written document detailing the terms of a business partnership.

A partnership is a business arrangement where two or more individuals share ownership in a company and agree to share in their company’s profits and losses. [1]

A simple Partnership Agreement will identify the following basic elements:

Before signing an agreement with your partner(s), understand a partnership’s advantages and disadvantages.

There are three main types of partnerships: general, limited, and limited liability. Each type impacts your management structure, investment opportunities, liability implications, and taxation.

There are also other variations, such as:

Any arrangement between individuals, friends, or families to form a business for profit creates a partnership. As there is no formal registration process, a written business partnership agreement intends to form a partnership.

It also sets out in writing the critical details of how the partnership will run.

Investors, lenders, and professionals often ask for an agreement before allowing the partners to receive investment money, secure financing, or obtain proper legal and tax help.

A general Partnership Agreement should generally have details outlining at least the following:

Here are some other valuable details an agreement might include:

You must also register your partnership’s trade name (or “doing business as” name) with the appropriate state authorities.

Yes, you can change, add or remove terms from a Partnership Agreement using a Partnership Amendment.

Reasons to change an agreement include situations such as additional investments or a requirement for more or new specific provisions to govern the partnership.

Writing a Partnership Agreement doesn’t have to be complicated; follow these steps:

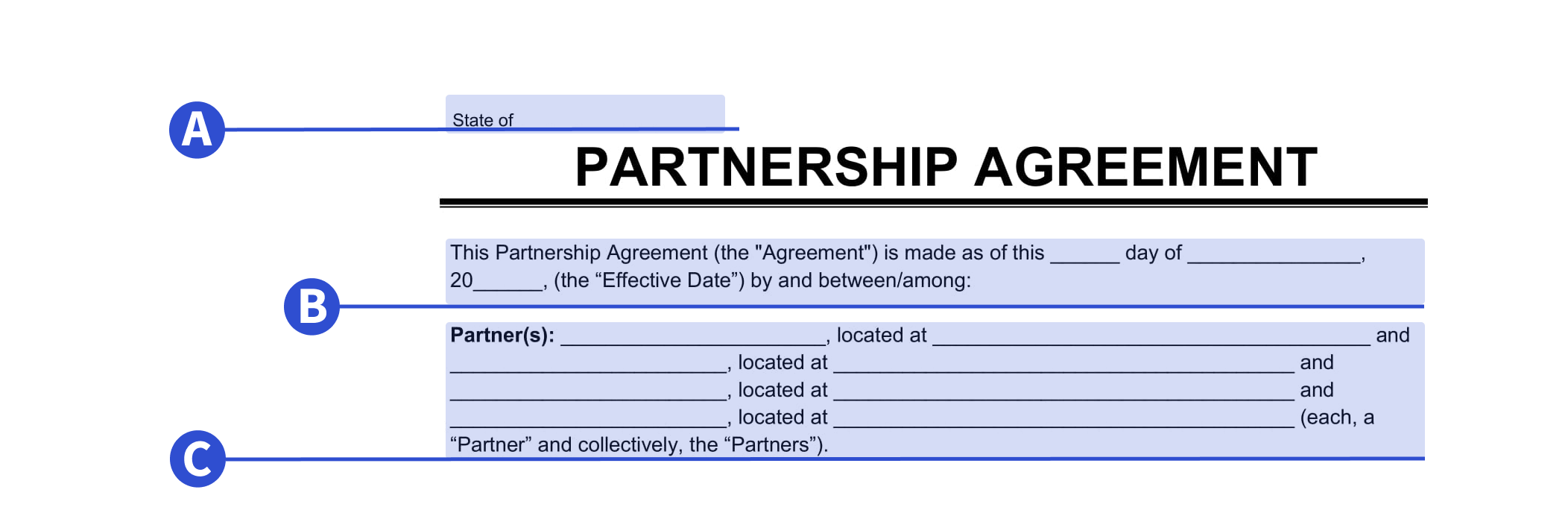

a) List the state governing the agreement

b) List the date the agreement was signed

c) List partner names and complete physical addresses

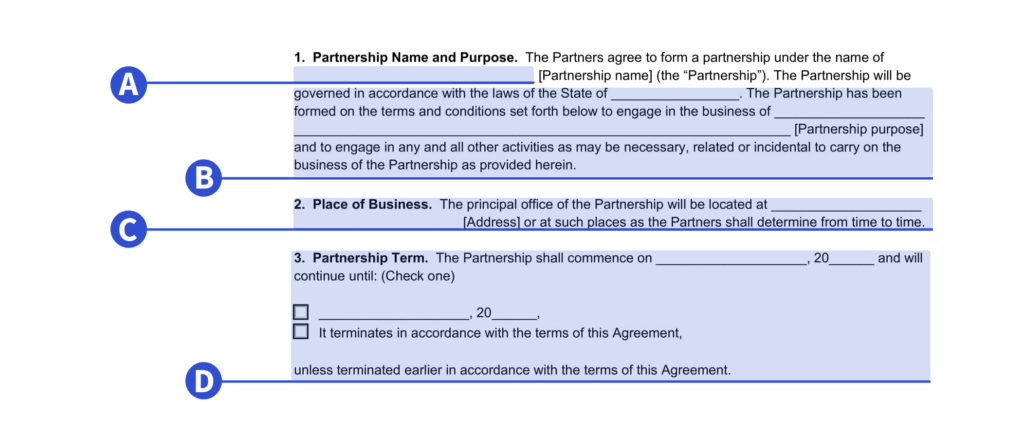

a) Provide the complete legal name of the partnership entity. It should be the name you have registered with your appropriate state department. If you have not formally created your legal entity, check with your state to ensure that the name you are using is available and check to be sure that you are not infringing on any existing trademarks.

You may also want to file with the state to reserve the name.

b) Describe the purpose of your business and list the types of business activities you will be engaged in.

c) This is the address where the business will operate and conduct business. This should be a physical address, not a PO Box. If you have registered your business with your state, you should provide the address you used in that filing here.

You can use a personal address if you are a completely virtual business without a physical business address.

d) Provide the date that the partnership will become effective. This can be done immediately upon signing this document or later. If you have a specific date for the partnership to end, you will list it here.

Otherwise, you will choose the preceding option, and the partnership will terminate upon the happening of events and as prescribed in the partnership agreement.

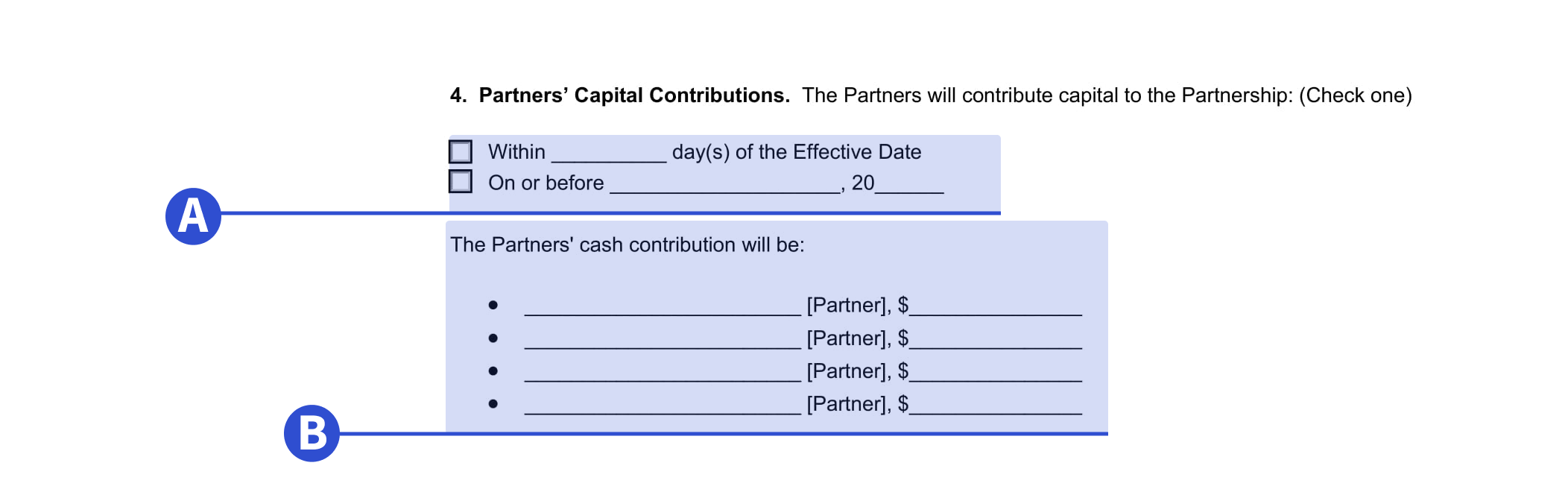

a) If partners are required to make capital contributions to the partnership, you must state when those contributions should be made here. You can choose when contributions should be received (for example, within 30, 60, or 90 days of the effective date of this agreement or on or before a set date).

b) Contributions are how much and what each partner will invest. They can be in the form of cash, property services, or expertise. You will list the number of contributions and describe the contributions here.

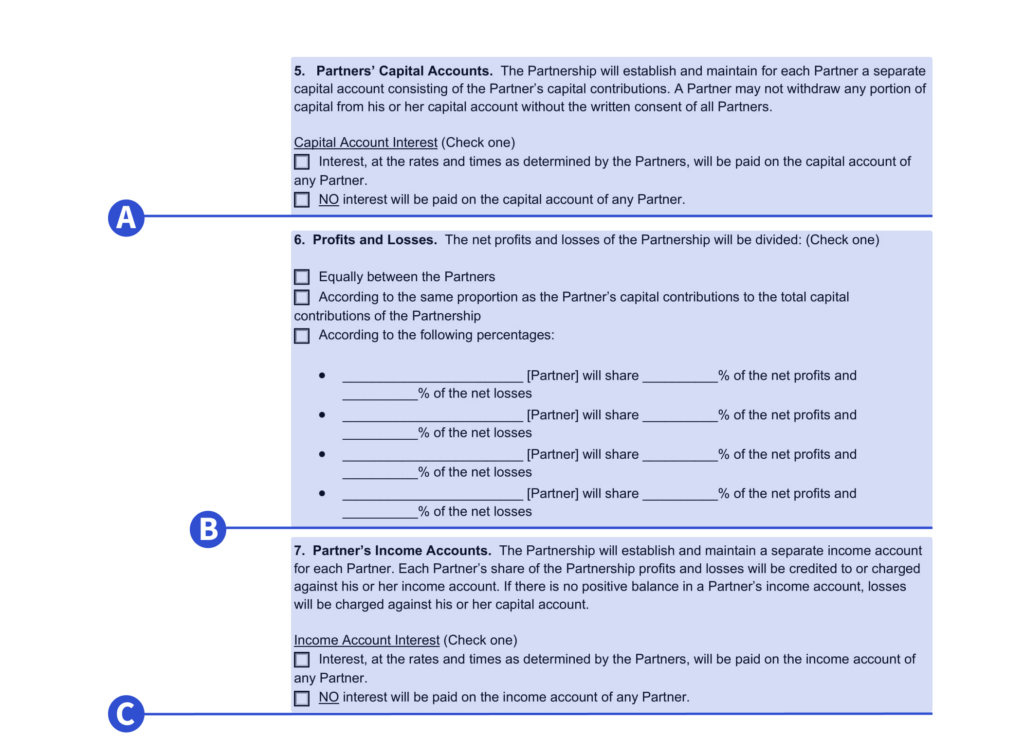

a) Capital accounts can pay out interest. You can decide whether the partners’ capital accounts will or will not pay out interest to any, all, or none of the partners depending on specific partner contributions and/or the goals and operations of your business.

b) Depending on each partner’s initial and future contributions, you can choose to divide profits and losses:

Partners can also choose to distribute the profits at a different ratio than the losses.

c) Each partner will have a separate income account. The partner’s share of profits and losses will be credited to or charged against. You can choose whether interest will or will not be paid to any, all, or no partners here.

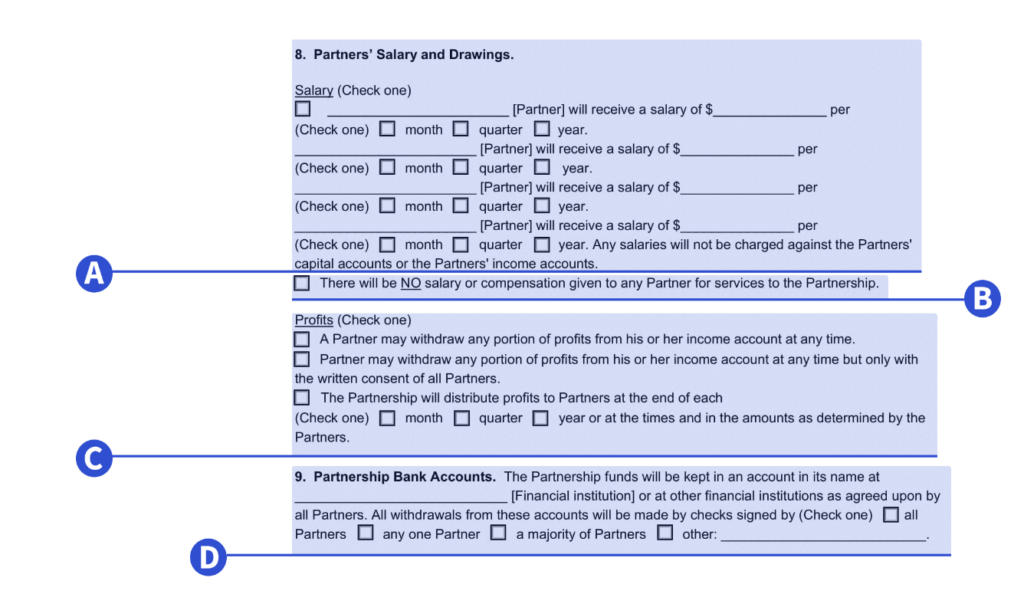

a) Partners can receive a salary for their labor and services. It is essential to consider the partnership’s profits, the goals of the partnership, and the partners’ contributions when determining salary.

The IRS considers a partner to be an employee only if the partner provides services other than their capacity as a partner, which could affect how both the partnership and the partner are taxed.

b) Choose this option if no salary will be provided to any partner.

c) Choose how partners can withdraw their profits from their income account here, either withdraw anytime, with written consent from all other partners, or at the end of a set period (monthly, quarterly, or yearly).

d) Provide the name of the financial institution where partnership funds will be held and list who can withdraw and sign on behalf of the partnership on this account.

It can be all partners, anyone partner, a majority of partners, or another arrangement you have decided upon.

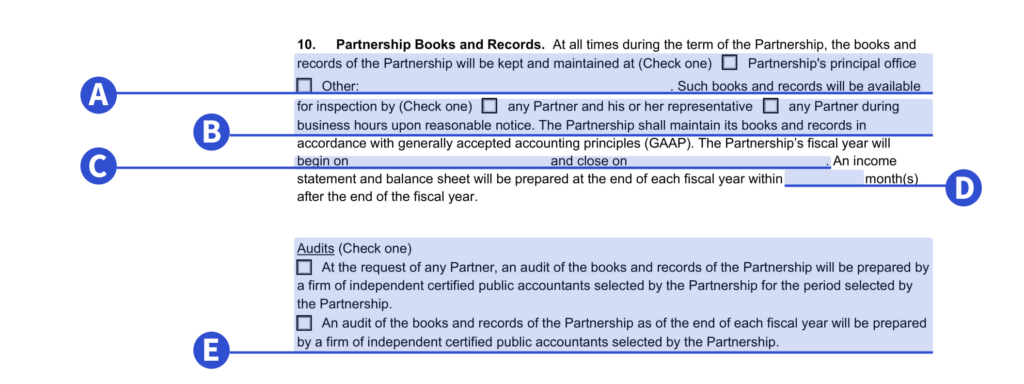

a) This is the physical address where books and records will be stored. This can be at the partnership’s principal place of business or elsewhere, like with a lawyer or CPA.

b) Choose who can inspect the books and records, any partner and their representative, or any partner.

c) List the partnership’s fiscal year. Most businesses will follow a calendar year, but you can choose any date for the beginning and end of your fiscal year.

d) This is at your discretion but typically occurs within a few months. You want to be aware of state or federal deadlines that may require this information when deciding the deadline to prepare the statement and balance sheet.

e) Choose when audits can be performed at a partner’s request or the end of the fiscal year.

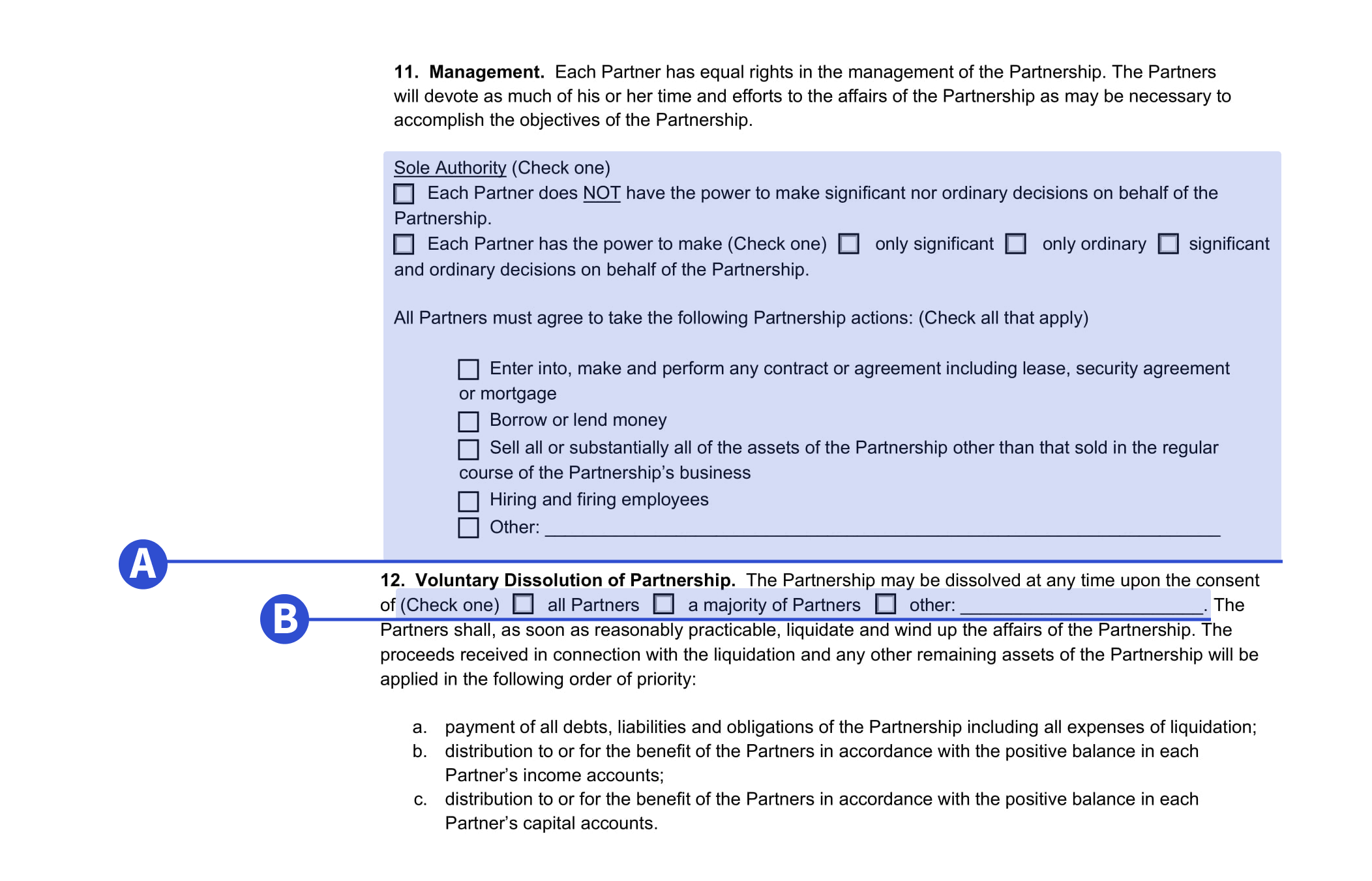

a) You can decide to allow each partner the sole authority to make decisions on behalf of the partnership. If you want to limit this authority, you can restrict this decision-making authority to only significant or ordinary choices.

A partner can decide on behalf of the partnership or bind the partnership to a contract without consulting the other partners.

b) You can choose to have the partnership dissolved upon unanimous consent of the partners or another event. It is standard to liquidate and wind up the partnership’s affairs and distribute any remaining proceeds upon dissolution.

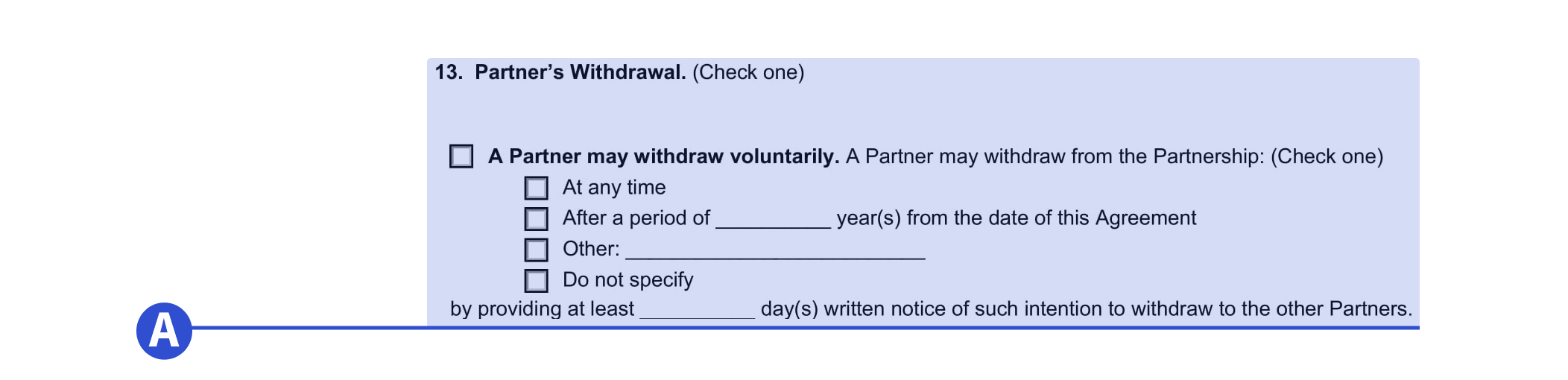

a) There are several ways a partner can leave the partnership. You can allow them to leave at any time or only after a certain number of years by providing a certain number of days’ notice. Or you can enable them to go only with the unanimous consent of the other partners.

Once a partner leaves, you can have the partnership automatically terminated, allow the other partners to purchase the interests, or give them the option to choose between both.

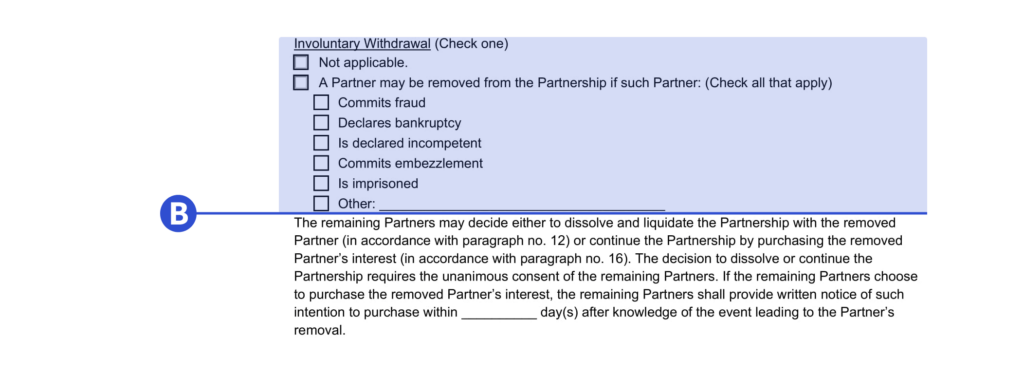

b) At some point, the partnership may decide that a specific partner’s actions are so harmful and detrimental to the partnership they need to be removed.

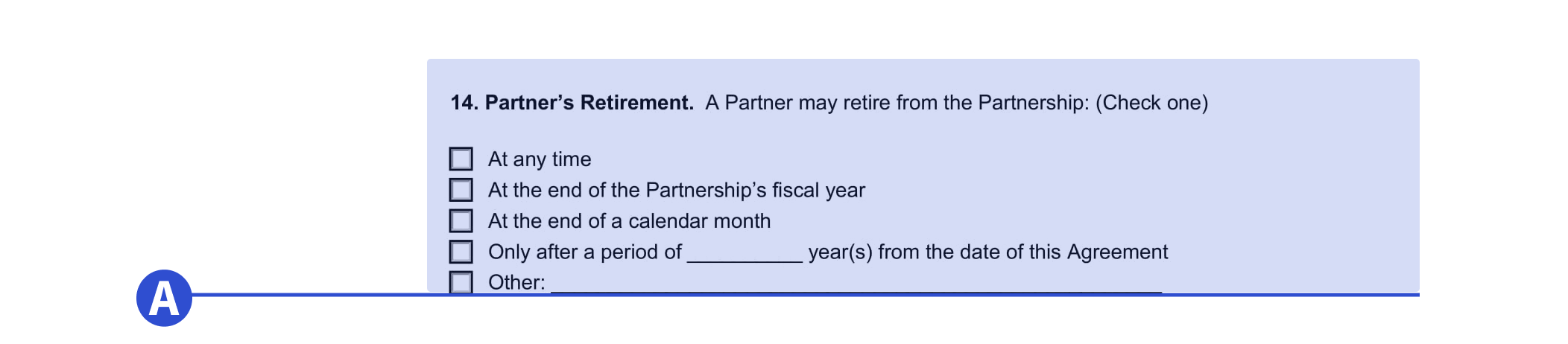

a) A partner may choose to retire from the business before the end of the partnership. You can allow a partner to withdraw or require retirement at a specific time.

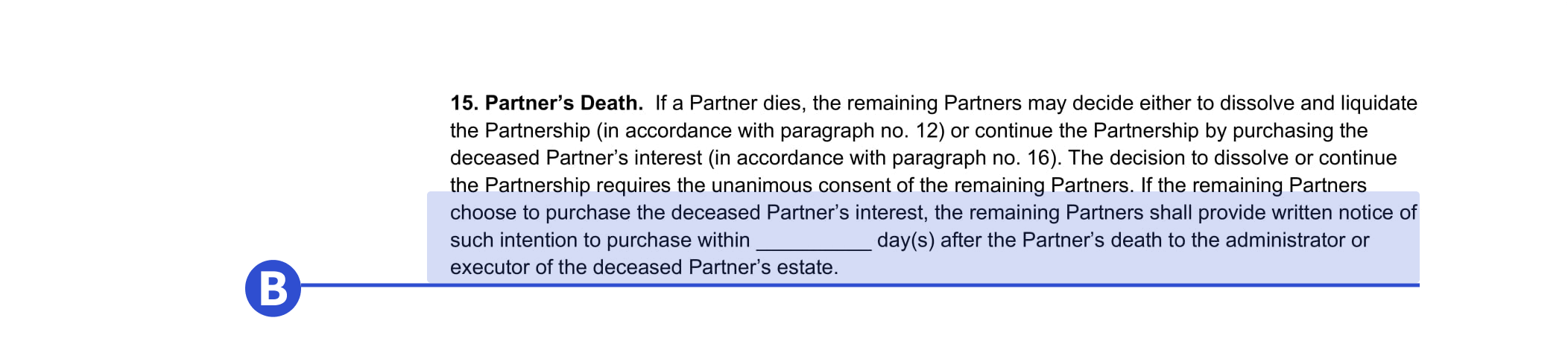

b) List the time allotted to provide written notice of intent to purchase the remaining partners of the deceased partner’s interest after death—for instance, 14 days.

a) The buyout price is the price the partners must pay for the withdrawing, retiring, or deceased partner’s interest.

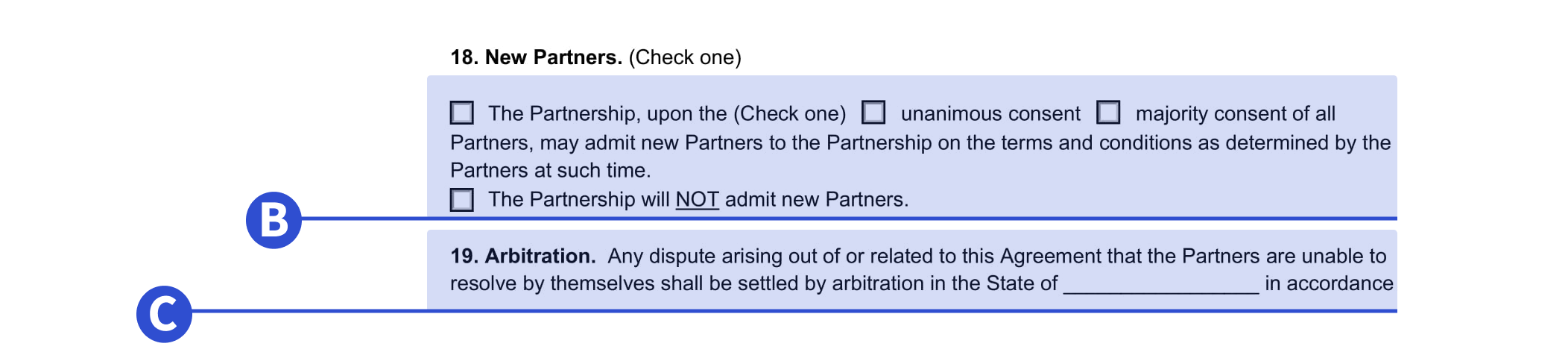

b) Your Partnership Agreement can specify that no new partners will be admitted to the partnership at any time or that new partners will be admitted to the partnership upon the agreement of the current partners.

c) All parties agree to resolve disputes over the agreement by arbitration. Arbitration is when an arbitrator, a neutral third party selected by the parties, evaluates the dispute and determines a settlement. The decision is final and binding.

Choose the state in which you would like any arbitration hearing held. Typically this will be the state governing this agreement.

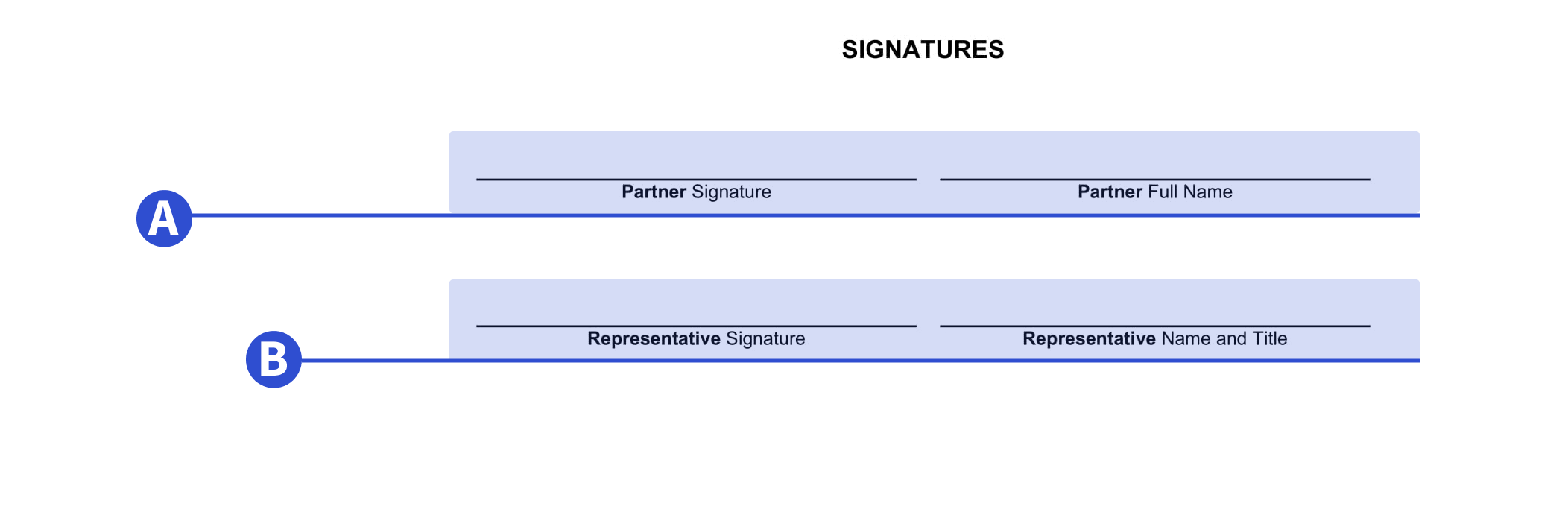

a) Partner signature and full name

b) Representative signature and full name.

The below partnership agreement sample shows you what a typical agreement looks like: